Chain but Owned by Different People I Will Not Be Going to This One Again

By Susan Helper and Evan Soltas

These are times of rapid transition for the U.S. economy. With the winding down of the worst of the pandemic, businesses have added jobs at a rate of 540,000 per month since Jan. Many consumers are making large purchases with savings accumulated during the pandemic, sending new home sales to their highest level in 14 years and motorcar sales to their highest level in 15 years.

While a fast pivot to growth is expert news for businesses and workers, it as well creates challenges. Entire industries that shrank dramatically during the pandemic, such every bit the hotel and restaurant sectors, are now trying to reopen. Some businesses written report that they have been unable to hire speedily enough to keep pace with their rise need for workers, leading to an all-time tape 8.iii million task openings in April. Others do non have enough of their products in inventory to avoid running out of stock. The state of affairs has been especially difficult for businesses with complex supply bondage, every bit their production is vulnerable to disruption due to shortages of inputs from other businesses.

These shortages and supply-concatenation disruptions are significant and widespread—only are likely to exist transitory. Below, nosotros describe the disruptions, the means that supply bondage have adapted to disruptions in the by, and how the Administration is working to address both brusk- and long-term supply concatenation issues.

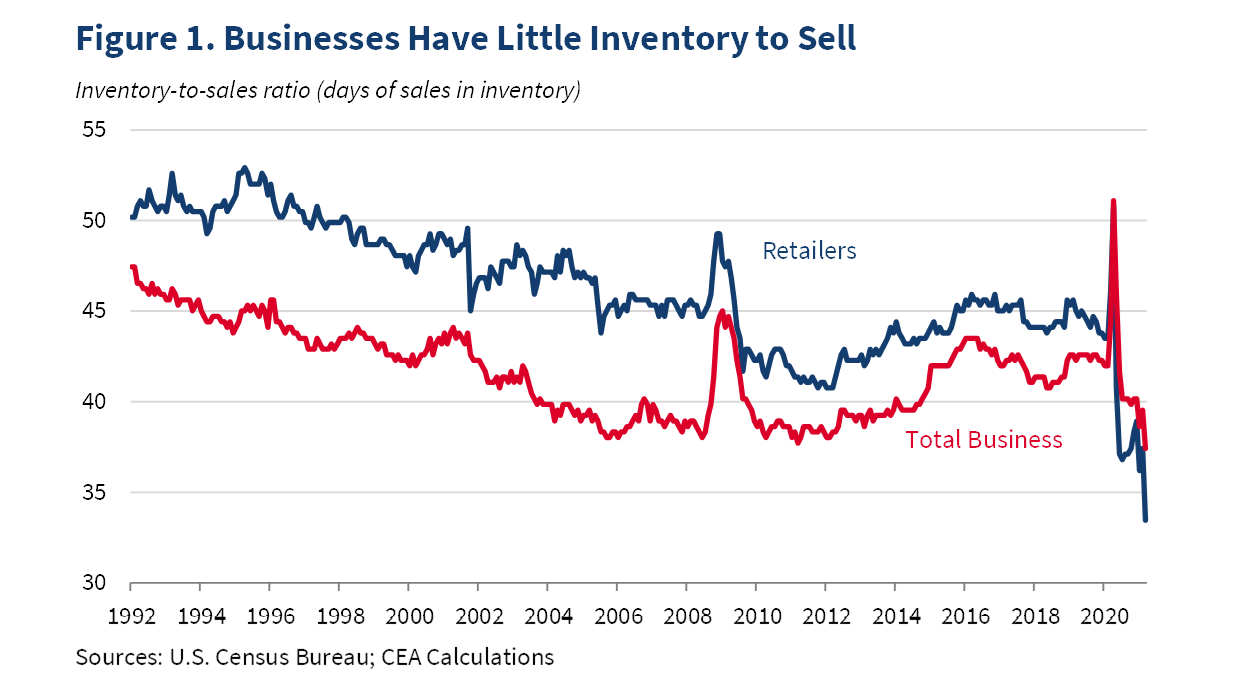

Effigy 1 shows that both the economy-wide and retail-sector inventory-to-sales ratios hit record lows in March. These ratios measure how many days of current sales that businesses and retailers could support out of existing inventories. When the pandemic hit, businesses were stuck with billions of dollars in unsold goods, causing inventory-to-sales ratios to surge briefly earlier businesses liquidated these inventories. But, as the economy recovered and need increased, businesses have not yet been able to bring inventories fully back to pre-pandemic levels, causing inventory-to-sales ratios to fall.

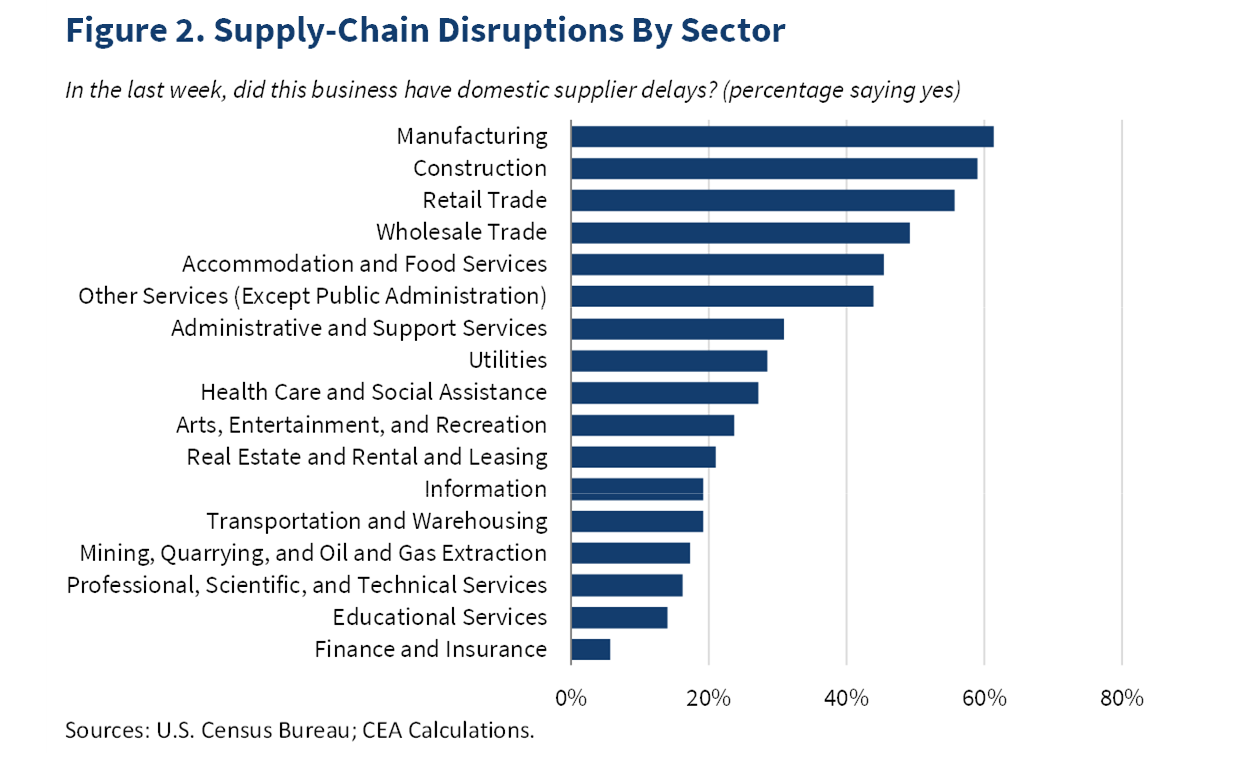

The figure shows that while retailers had 43 days of inventory in February 2020, today they have just 33 days. Inventories of cars and homes are as well at or about record lows, sufficient for only 1 month of car sales and 4.4 months of domicile sales, as compared to pre-pandemic levels of well-nigh two months for cars and 5.five months for homes. These depression inventories have caused cascading problems in industrial supply bondage. In the latest U.Due south. Census Small Business Pulse survey, held from May 31 to June 6, 36 percent of small businesses reported delays with domestic suppliers, with delays concentrated in manufacturing, construction, and trade sectors, every bit shown in Figure 2. While no comparable survey data be from before the pandemic, industry-specific surveys on input shortages suggest these levels are much higher than usual.

Data also suggest these shortages are holding back business action in some sectors. A record share of homebuilders, surveyed past the National Association of Homebuilders in May, reported shortages of key materials such equally framing lumber, wallboard, and roofing. Homebuilders appear to be responding to these shortages in part by delaying new construction, every bit housing starts accept been volatile for several months.

Another impact of the shortages has been abrupt toll increases. Betwixt May 2020 and May 2021, prices of commodities tracked within the Producer Price Alphabetize rose by 19 percent, the largest yr-over-year increase since 1974, in part reflecting base effects. Some increases accept been especially dramatic. Facing a shortage of lumber, homebuilders briefly sent prices to $one,711 per thousand board-anxiety terminal month, an corporeality that implies a typical 2,000-foursquare-human foot house would require more than $27,000 in framing lumber alone, relative to a lumber nib of about $7,000 before the pandemic.[i] Lumber prices have now rapidly come up back down, falling 38 percent from their record high, in an early sign that some shortages may be short-lived.

Supply-concatenation disruptions are likewise having a material impact on consumer prices, especially in the motor vehicle sector. Over half of the May increase in core inflation as measured by the Consumer Price Alphabetize comes from this sector, if nosotros include prices of new, used, leased, and rental automobiles. This sector too accounted for one-third of the economy-broad increase in prices compared to a yr ago.[two]

A key reason for the astute problems in motor vehicles is that automakers appear to take underestimated demand for their products subsequently the beginning of the pandemic. Expecting weak demand, they cancelled orders of semiconductors, an item with a long lead fourth dimension and with a secular increase in demand from other industries. This problem is compounded past the fragmentation in recent decades of the motorcar supply chain across many countries and many firms. This phenomenon has fabricated it hard for automakers to trace the root causes of bottlenecks, since for example a semiconductor may be designed past i firm, manufactured by a second firm, embedded into a component (such every bit an air handbag) by a third supplier, and only then delivered to an automaker's associates plant. In most cases, neither the automaker nor the semiconductor manufacturer can trace what goes on in these intermediate layers (or "tiers") of the supply chain, due in part to lack of trust amid parties in supply chains, who fear that the data might be used to replace them or to bargain for a toll reduction. While these problems are near acute in semiconductors, they are institute in other parts of the car supply chain likewise. The auto sector is "the manufacture of industries," so the price of cars is affected by the prices of the 30,000 parts in the car, from semiconductors to steel to plastic to condom, and the logistics of transporting these parts across multiple national borders.

While the economy-broad nature of these shortages is unusual, the history of supply disruptions in specific industries may offering insights equally to how the shortages volition be resolved over time. In the past, many industries have been surprised by strong demand and defenseless with besides picayune inventory of specific goods. Others take been hit with a supply stupor due to a crop failure or a natural disaster which took key factories temporarily offline, such as after the 2011 earthquake in Japan. In many such cases, markets made their manner back to equilibrium relatively quickly.

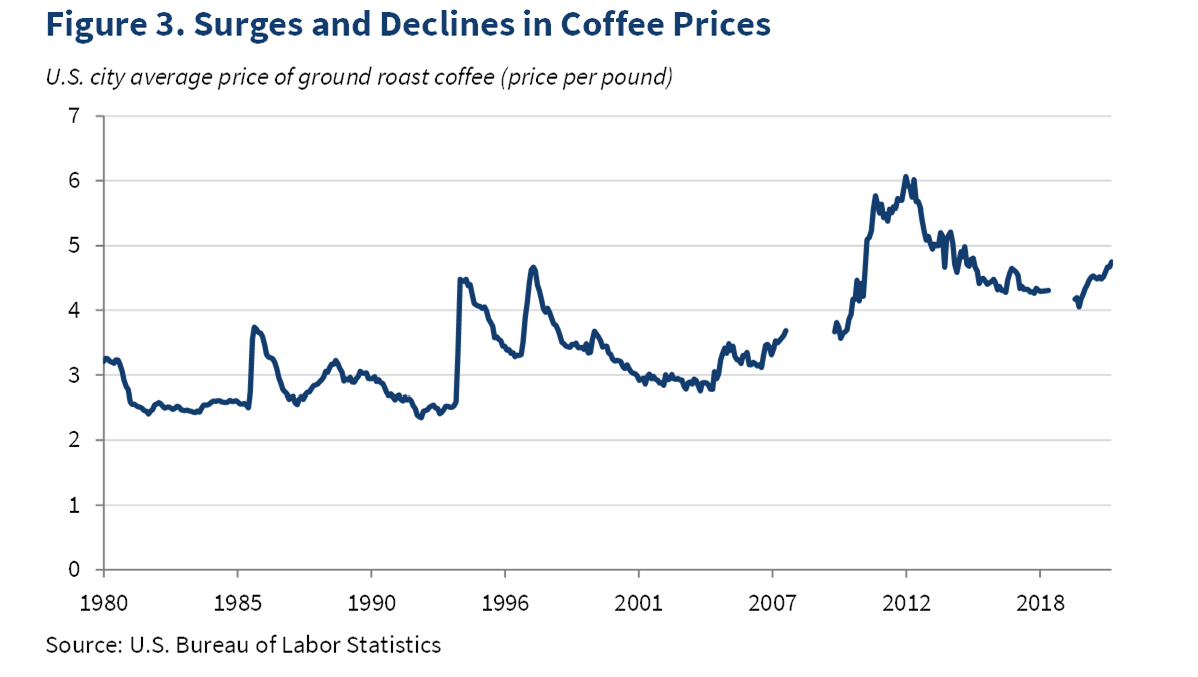

Take java, for example. Every bit some coffee drinkers can retrieve, coffee prices have spiked repeatedly due to frosts that damage coffee harvests, most recently in late 2010. Each fourth dimension, the weather normalized, harvests improved, and prices fell dorsum towards their previous levels. Similar transitory price spikes have occurred in markets for agricultural goods and other commodities—peanut butter amid a drought in 2011, or eggs amid an outbreak of bird flu in 2015.

The toilet-newspaper shortage in the early days of the pandemic offers another useful instance report. Stay-at-dwelling house orders led to a sudden 40-percent increment in need for retail toilet paper, the fluffier kind used by households. Yet supply cannot rise overnight to satisfy demand. Toilet newspaper is bulky to store, and demand is ordinarily very stable, which led retailers to go on just 2 to 3 weeks of sales in inventory and manufacturers to operate their plants at 92-pct capacity. Worried they would be left without toilet paper, Americans cleaned out store shelves.

How did U.Due south. toilet-paper manufacturers respond to the shortages? None announced to have added production lines or built new plants to aggrandize capacity. That is because the modern toilet-paper manufacturing process is highly mechanized and capital-intensive, requiring four-story-alpine machines that cost billions of dollars and months to get together before a single curlicue comes off the line. And few announced to have converted factories from scratchier commercial toilet paper to retail varieties, unlike the rapid retoolings that allowed U.Due south. manufacturers to ramp upwardly production of cleaning wipes and paw sanitizer. Nor did many sell commercial toilet paper to households.

Instead, manufacturers wrung a scrap more out of their existing processes. They ran plants at nearly 100-pct capacity and restarted idled mechanism. Some streamlined their product offerings, reducing auto downtime and, in particular, shifting to big-whorl products that could go more paper to households without costly changes to machinery. Others invested in their distribution systems, then that they could anticipate and reply more quickly to local shortages.

These resilient responses from manufacturers helped to shorten the stressful menstruation of empty store shelves.

There is evidence indicating that the current disruptions are likely to exist more often than not transitory. Indices of current delivery times are at tape highs in surveys of manufacturers by three regional Federal Reserve Banks, only Fed indices for futurity delivery times are in their typical ranges. While current indices study conditions at the time of the survey, the time to come indices study expectations about conditions in half dozen months. Taken together, the data suggest that manufacturers conceptualize current supply-chain problems will have abated inside six months or so.

While markets will somewhen adjust, they tin be slow and the impact on producers and consumers can be costly. The public sector can play a valuable role in reducing these costs by facilitating short-term adjustments and by addressing vulnerabilities in U.S. supply chains. The U.Due south. regime has, at critical moments, provided such support: helping Japan respond after the 2011 earthquake, for example, or producing COVID-19 vaccines through Operation Warp Speed. Last week, the Biden-Harris Administration released the conclusions of its 100-day review of supply chains for four disquisitional products: semiconductor manufacturing and advanced packaging; large capacity batteries, like those for electrical vehicles; disquisitional minerals and materials; and pharmaceuticals and agile pharmaceutical ingredients. Guided past these reviews, the Administration will act to address both brusk-term strains and long-term vulnerabilities, such equally those due to excessive concentration of production of key inputs in a few firms and locations.

The Administration has established a Supply Chain Disruptions Task Force to monitor and address brusk-term supply problems. This Chore Strength is convening meetings of stakeholders in industries with urgent supply-chain problems, such equally construction and semiconductors, to identify the immediate bottlenecks as well as potential solutions.

For the longer term, the Assistants proposes a variety of actions to strengthen our industrial base, increasing resilience and reducing lead times to reply to crises. Information technology vows to opposite long-time policies that have prioritized low costs over security, sustainability and resilience. Because these policies ignored the costs of being unprepared for risk, the United States has ended upward with brittle supply chains that are, adjusted for the costs associated with this take a chance, also quite expensive. The Administration proposes to reverse this harm by investing in inquiry, production, workers, and communities that will rebuild sustainable manufacturing capacity beyond the country. In particular, the Administration recommends that Congress support at least $fifty billion in investment to accelerate domestic semiconductor manufacturing and research. Another proposed action would accost international vulnerabilities to supply bondage. Considering information technology does not brand sense to produce everything at abode, and because U.S. security also depends on the security of our allies, the United states must piece of work with its international partners on commonage approaches to supply chain resilience, rather than being dependent on geopolitical competitors for central products.

Restarting the economy afterwards a pandemic and a recession has not been and will non be simple. Hundreds of thousands of small and large businesses take to reopen, millions of laid-off workers have to find new employers, and manufacturers have to bring dorsum product lines idled during the pandemic. Such changes have time. The Biden-Harris Administration is working to speed up the resolution of these transitory shortages and supply-chain disruptions—to make our supply bondage more resilient to futurity shocks and to build back ameliorate,.

[1] Calculations assume xvi,000 lath-feet of framing lumber in the house.

[ii] "Cadre inflation" is a measure that removes from the toll alphabetize those products, like food and energy, whose prices are normally volatile.

Source: https://www.whitehouse.gov/cea/written-materials/2021/06/17/why-the-pandemic-has-disrupted-supply-chains/

{kind=link}

Post a Comment for "Chain but Owned by Different People I Will Not Be Going to This One Again"